Intel Corporation is one of the largest semiconductor chip makers in the world. The company’s stock has struggled in recent years due to declining PC sales, production delays, increased competition, and other challenges. Many investors are questioning if Intel stock will recover or continue to decline.

What Does Intel Produce?

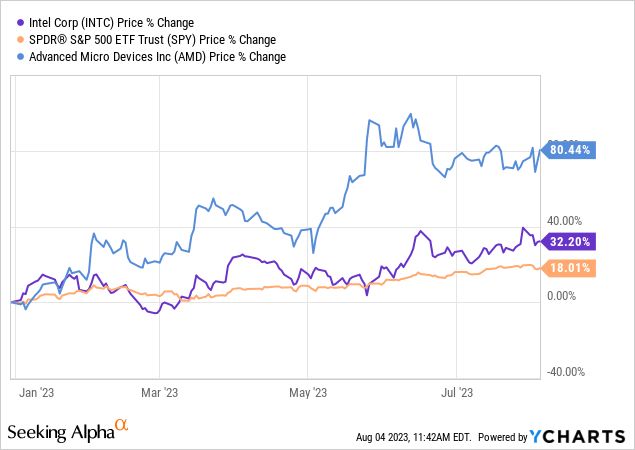

Intel is best known for its PC central processing units (CPUs) like the Core i3, i5, and i7 processors. The company has dominated the PC CPU market for decades, though its market share has declined in the face of competition from Advanced Micro Devices (AMD).

In addition to PC CPUs, Intel also produces:

- Server and data center processors

- Embedded and Internet of Things (IoT) processors

- Memory and storage products

- Programmable semiconductors (FPGAs)

- Autonomous driving tech

- 5G networking components

Intel’s product portfolio remains robust, though the decline in PC sales has severely impacted parts of Intel’s business. The data center segment continues to provide strong growth for the company.

Why Has Intel Stock Declined?

Intel’s stock has faced several challenges in recent years contributing to its decline:

Falling PC Sales

The PC market has contracted significantly from its peak in the early 2010s. Consumers are holding onto devices longer and increasingly shifting to smartphones and tablets. Fewer PCs means reduced demand for Intel’s PC CPUs.

Manufacturing Delays

Intel has faced delays in transitioning to newer, smaller transistor manufacturing processes. For example, the rollout of the company’s 10nm process node was significantly delayed compared to competitors. This has hurt Intel’s ability to increase performance and efficiency.

Increased Competition

Intel is facing renewed competition from companies like AMD and Qualcomm. AMD has been chipping away at Intel’s market share in both the consumer and data center CPU markets. Competition has placed downward pressure on prices and margins.

Executive Turnover

In the past several years, Intel has dealt with significant executive turnover including the departure of its CEO, CFO, and various other senior leaders. The lack of consistent leadership has contributed to Intel’s challenges.

Security Vulnerabilities

Major security flaws like Spectre and Meltdown have also impacted Intel. While not unique to Intel, the vulnerabilities highlighted risks in the company’s CPU designs. Intel has had to allocate significant resources to patching security issues.

Will New Management and Strategy Lead to Recovery?

In early 2021, Intel appointed industry veteran Pat Gelsinger as its new CEO. Gelsinger outlined a strategy focused on:

- Improving Intel’s CPU manufacturing and process technology

- Competing more aggressively for market share

- Investing heavily in R&D to drive innovation

- Exploring foundry services to manufacture chips designed by other companies

Gelsinger aims to restore Intel’s reputation as the premier chipmaker. But this turnaround will take time. Intel plans to invest $25 billion in new factories to regain process leadership. But the payoff from these investments will take several years to materialize.

In the meantime, Intel faces tough competition from companies using the manufacturing capacity of Taiwan Semiconductor Manufacturing Company (TSMC). TSMC’s smaller process nodes have allowed AMD, Apple, Qualcomm and others to surpass Intel’s chip performance. Intel is still playing catchup.

How is Intel Performing Financially?

Revenue and Market Share

Intel’s revenue declined modestly from $77.9 billion in 2018 to $73.9 billion in 2021. However, competitors like AMD, Apple, and Qualcomm are steadily capturing market share in key segments including PCs, mobile devices, and data centers. Intel’s market share loss presents risks to long-term revenue growth.

Profits and Margins

Despite revenue headwinds, Intel has sustained relatively strong profitability:

| Year | Net Income | Profit Margin |

| 2018 | $21.1 billion | 27% |

| 2019 | $21.0 billion | 27% |

| 2020 | $20.9 billion | 24% |

| 2021 | $19.9 billion | 26% |

Though margins remain relatively high, they have slipped in recent years due to competitive pressures. Maintaining profitability while attempting to regain market share will be a challenge.

Free Cash Flow

Intel continues generating strong free cash flow, giving it flexibility to fund capital expenditures and R&D needed for its turnaround. The company produced free cash flow of $21 billion in 2020 and $19 billion in 2021. Cash flow funds Intel’s huge investments in new fabs and process improvements.

What Potential Risks Does Intel Face?

Challenges that could further hamper Intel stock include:

Loss of Market Share

If Intel continues ceding market share to AMD, Apple, Qualcomm and other competitors, it risks permanent revenue declines and margin erosion. Dropping demand for Intel’s CPUs would severely damage financial results.

R&D and Manufacturing Investments

Intel’s plan to spend tens of billions upgrading factories and recovering its process lead won’t pay off immediately. In the interim, cash flow and earnings could suffer under the weight of huge capital expenditures if Intel fails to regain market share.

Foundry Business Challenges

Becoming a foundry that manufactures chips for other companies is a new business for Intel. This carries risks as its foundry efforts will compete against pure-play foundries like TSMC and Samsung. Intel could face challenges establishing its foundry business.

Execution Setbacks

If Intel experiences further delays or missteps in product development, manufacturing, or technology, it could extend the company’s turnaround time. Previous execution issues have contributed to Intel’s current predicament. More setbacks could worsen competitive threats.

What Potential Catalysts Could Boost Intel Stock?

Some developments that could propel an Intel stock price recovery include:

Regaining Process Leadership

If Intel can beat competitors to market with new manufacturing nodes and make rapid progress developing advanced packaging innovations, it could reclaim its process advantage. This could drive big performance and efficiency gains.

Launching Breakthrough Technologies

Intel is investing heavily in areas like GPUs and AI. If the company could lead in launching revolutionary new technologies and products, it could claim new markets the way it originally dominated CPUs.

Growth in Data Center, IoT, 5G Markets

Strong growth in data centers, Internet of Things (IoT), 5G networks and other markets Intel targets represents upside. Gaining share in these expanding segments would boost Intel’s revenue.

New Customer Wins

Major customer wins for Intel’s foundry business, such as manufacturing chips designed by Apple or Qualcomm, would demonstrate strong demand. This could become a meaningful 2nd business for Intel over time.

Conclusion: Intel Faces Difficult Path to Recovery

In summary, while Intel maintains financial strength, its path to reversing market share losses and re-establishing process leadership remains challenging. The company’s new CEO has laid out an aggressive strategy to compete, but Intel realistically faces years of tough slogging.

In the near-term, Intel stock is unlikely to recover strongly until the company can prove it is making real technological progress. But for long-term investors, Intel still represents an important player in key IT markets with strong financial resources.

If Intel successfully navigates its multi-year turnaround, its stock could reward investors handsomely. But in the short-term, Intel faces too many competitive and technological headwinds to make a quick stock price recovery the likely outcome. Careful monitoring of Intel’s execution and financial metrics is warranted.